Can austerity be avoided?

Can austerity be avoided?

Or might it be even worse than planned?

Duncan Weldon makes the point well that while the prospect of fiscal consolidation is rather grim, Hunt has managed to walk the tightrope of managing to restore the Government’s fiscal credibility with the markets while not actually launching into cuts straight away. The graph below compares Osborne’s austerity plans to the new spending plans in real terms. You can see that the consolidation isn’t due to start until 2025:

Of course some of this is political. They don’t want to cut until after the next election (most likely to happen in 2024 and by the end of January 2025 at the latest) but it does at least give a chance for conditions to change, allowing for less austerity, or none at all.

Hunt hasn’t left himself much margin for error. He only has £9.2bn to play with, of which he is likely to lose about £5-6bn when they inevitably u-turn on the planned fuel duty increase at the next Budget. There is not much ‘free’ money lying around.

But austerity (at least of the scale planned) isn’t inevitable. There are a couple of easy ways to avoid this mess:

#1 Avoiding austerity through higher net migration (quite likely)

The easiest way for the UK to avoid austerity is for net migration to consistently overshoot the OBR forecast by a large amount.

While the latest OBR forecast has already adjusted up the net migration assumption used in the modelling, there are reasons to think that net migration could consistently overshoot even this new estimate.

For a start, the latest ONS figures last week showed net inwards migration of over 500k in the year up to June, more than double the OBR forecast:

Second, despite Brexit ending freedom of movement, the UK (as a consequence of the post-Brexit visa regime) still has one of the most liberal migration regimes of any developed country. More than half of all jobs in the UK are open to anyone from anywhere in the world (although there is of course a paperwork cost for employers).

Third, the UK is still an incredibly attractive place for migrants given the use of English and the large pre-existing migrant populations.

While some of recent jump in net migration may just be people who couldn’t come during the pandemic now making the move over as well as a couple of one-off flows (Ukraine + Hong Kong), I suspect, for the reasons above, that net inwards migration will consistently overshoot OBR assumptions in the forecast period. If it does, that should give a welcome boost to GDP helping the public finances (the impact on GDP per capita will, however, be much much smaller).

#2 Avoiding austerity through a closer trading relationship with the EU (very unlikely)

The other ‘easy’ way to increase output over the forecast is to have a closer and more stable trading relationship with the European Union. Over the longer term I am optimistic that this will happen but I’m less sure over the next five years or so for a few reasons.

First, the Government doesn’t have the appetite to substantially change its approach, and couldn’t even if it wanted to because of Tory backbench opposition. The government will be more constructive with the EU but I suspect this will not translate into any substantive changes to trade policy.

Second, while Labour are clear favourites to win the next election, their route to a majority relies on winning the so-called ‘red wall’ seats which tend to be more supportive of Brexit. Because of the SNP’s dominance in Scotland, these red-wall seats are a must win for Labour. As a result, they will continue with their commitments not to rejoin the EU Single Market, Customs Union or to bring back something like freedom of movement. A Labour Government which wins a second term in office may seriously consider a substantively different approach, but that’s all beyond the forecast period.

Beyond policy: rates and gas prices could impact the scale of austerity significantly

Beyond more direct policy levers on migration and Brexit the main short term variables that would dramatically impact the forecast are changes in natural gas prices and lending rates. These could then have a huge impact on the fiscal space available:

Gas prices are currently trading around 6x higher than pre-crisis levels. If prices come down closer to pre-crisis levels more quickly than expected then trend output could be increased by up to 0.6-0.7% (taking the OBR estimate that a 10% increase in gas prices reduces potential output by 0.1%).

Being positive, market structures that created huge price spikes over the summer are being smoothed over with new regulation. There has been a significant push to diversify away from Russian gas and more of a focus on energy efficiency and alternative forms of power. It’s therefore possible that gas and/or other energy prices come down quicker than expected.

On a more negative note, even if efficiency savings and cheaper energy can be brought on stream, this is unlikely to happen quickly enough to avoid the start of the cuts. There is also a risk of cold winters and further disruption to gas supply chains (e.g. sabotaging of gas pipelines as with Nordstream). And, even if the war does finish soon, Europe is not going to shift back to a reliance on Russian gas.

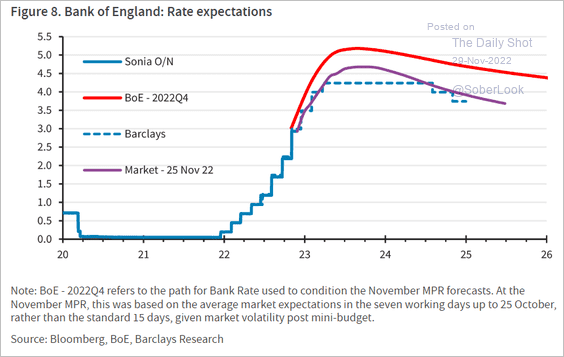

Rates could undershoot the market expectations used in the OBR forecast. Market expectations of the Bank rate are already an average of 0.5 ppt lower than the path used in the OBR model over the forecast period:

Very roughly, this might translate into an extra 0.2% of growth at the end of the forecasting period using OBR numbers. What’s more, the Bank has been trying to signal that they intend to keep rates lower than the market-implied numbers. Generally forecasts rather than OIS forward rates seem to agree with Bank’s assessment:

We do have to be careful here not to reason from a price change. Rates could be lower simply because growth is even weaker than expected. This is certainly a possible outcome if the global economy is worse (think no soft landing in America and China weakness) and energy prices are higher than expected over the period.

But, more optimistically, lots of the inflation should wash out of the numbers mechanically over the next year. If global conditions are relatively benign, the UK continues to attract migrants and/or firms find it easier than expected to adjust to Brexit then a softer landing in the UK with higher growth and lower rates is not totally inconceivable.