Modelling UK CPI for 2023

Setting some reasonable upper and lower bounds

I’ve created a basic model of UK CPI to get a better feel for how inflation will play out in 2023.

I’m not trying to model what will happen but simply to give a rough idea of upper and lower bounds conditioned on reasonable pessimistic and optimistic assumptions about consumer demand and commodity prices over the next year. There is a description of the model at the end of this piece for anyone interested.

Reasonable Worst Case (RWC) Scenario

Assumptions:

The Energy Price Cap goes up to £3,000 in April as planned with prices staying there throughout the year. This assumes that natural gas prices don’t stay low enough for long enough to bring the typical household cost below that £3,000 cap as some now forecast.

Actual rents grow by 5% over the next year (vs 4.7% annualised rate between December 2021 and December 2022). This is plausible as a result of higher mortgage rates…

(i) Pushing more people into the rental market

(ii) Owners of rental properties having to sell because of rising costs on their own mortgages which then lowers the available supply of rental properties

Petrol and diesel prices remain at current levels. This might be the case if some or all of the following happen:

(i) Increased demand from China raises wholesale prices

(ii) Less overall supply with no further releases from the SPR

(iii) Petrol Station owners not fully passing on any decreases in wholesale pricesAn increase in train ticket prices by 5.9% from March as announced by the Government.

A 4% increase in phone and internet bills. This is just from eyeballing what most suppliers are doing. (link)

Air travel costs stay at elevated levels (they are up 44% from December 2021).

Everything else grows at 2/3 of its 3m/3m (October to end of December) annualised growth rate. This can be thought of as 2/3 inflation ‘persistence’. For some things like food, this means a further annualised inflation of almost 14% while for other things - like second hand cars - this means a gentle disinflation. This assumption of strong inflation persistence is plausible if some or all of the following happen:

(i) Wage pressures remain stubbornly high, leading to a further round of price hikes

(ii) Slow passthrough from the original inflation shock. Businesses that held off on increasing prices in 2022 increase them in 2023

(iii) China reopening causes bottlenecks and increased commodity prices

(iv) UK labour market issues create problems for hiring in specific sectors

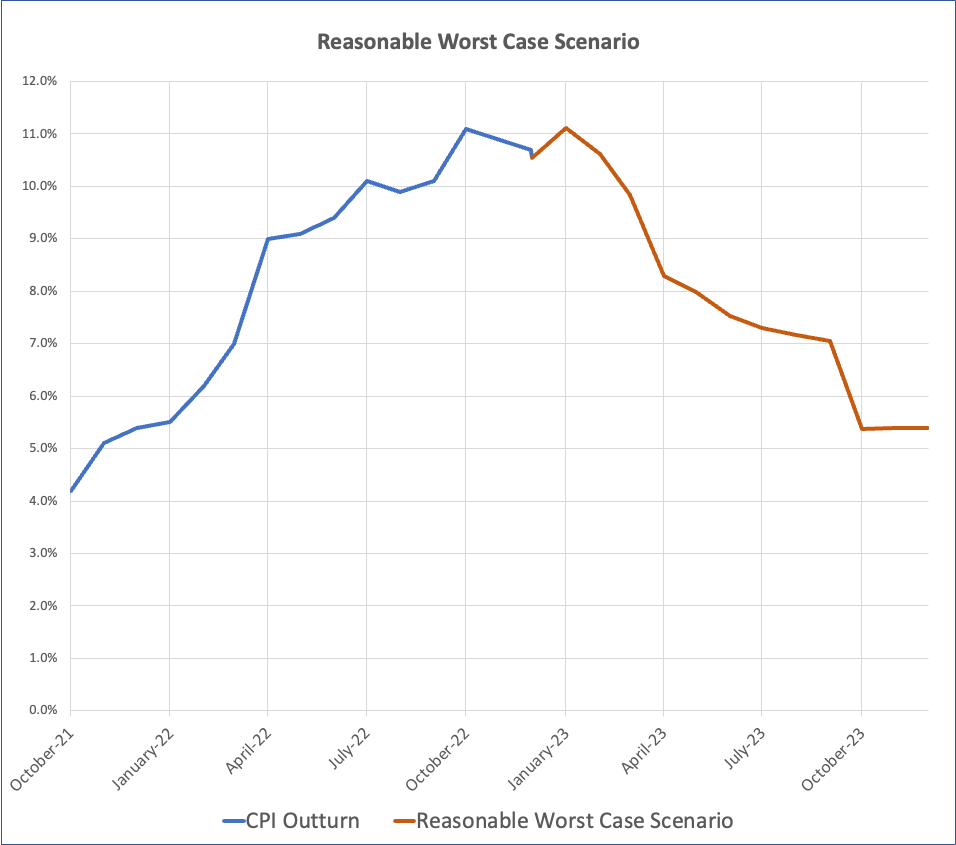

Plugging these assumptions in gives the following output:

As you can see inflation comes down but still ends the year above 5% - well above the 2% target.

And being ultra-pessimistic - here is a scenario assuming rents go up by 6% and 100% inflation persistence for food items:

Here inflation still comes down from its peak but ends the year above 6%.

Reasonable Best Case (RBC) Scenario

Energy Price Cap goes up to £3,000 in April for three months as the result of previous wholesale prices that now need to be passed on. But, from July, I’ll assume that gas futures continue to fall in price and that the typical household bill from then on out is 5% below the Cornwall Insight predictions of £2,800 for Q3 and Q4 (link).

An increase in rents of ‘only’ 3% which has been fairly typical over the past 20 years (link). This is possible because

(i) There has been a base effect of rental inflation being ‘too low’ during 2020 and 2021. This might now wash out of the numbers.

(ii) Last year saw a record amount of net inwards migration. Some of this might have been a one off adjustment after COVID which could have jolted the rental market upwards. The market might now readjust to a lower speed of price increases.Petrol and diesel prices gradually fall back to where they were in September 2021 by the end of 2023. This is plausible if energy prices continue to fall and if wholesale price decreases are passed on to the final consumer.

Inflation persistence of only 1/3 of the 3m/3m annualised growth rate for all other areas. This is plausible if …

(i) The economy slows creating less demand

(ii) Wage dynamics are fairly well anchored

(iii) There is no commodity price spike

(iv) Most of the passthrough from the energy price spike has already happenedRail, phone & internet, and air travel assumptions as in RWC scenario

With these assumptions we get this output:

This shows inflation basically returning to target by the end of the year.

How these upper and lower bounds fit with the professional forecasts

The table below collated by the Treasury shows a range of forecasts:

The midpoint of my RWC and RBC scenario is that inflation comes down to 3.85% by the end of 2023. The OBR prediction is 3.8% while the average of the forecasts made in January is 4.48%.

The highest of the predictions made in January is 6.8% by Beacon Economics. This is a little higher than the RWC+++ output where inflation sits at 6.3% at the end of the year. The lowest inflation prediction is 2.3% by Pantheon Macro which matches my RBC.

Conclusion

Assuming no extreme events, inflation is likely to fall roughly within this band:

The RBC involves a very steep decrease in inflation. To the extent that this is just energy and food price spikes washing out of the numbers this is a a very good thing. But if large parts of this fall are the result of demand destruction then it may be a sign that the Bank hiked rates too quickly and too far.

On the other hand, there isn’t much good that can be said about the RWC scenario which largely represents what might happen if there is another spike in energy/food and commodity prices. This wouldn’t just be bad in 2023 but is a huge risk for inflation expectations. Even if the economy is very weak, the Bank may feel that they have to raise rates further or keep them higher for longer simply to get expectations back into line.

How the model works

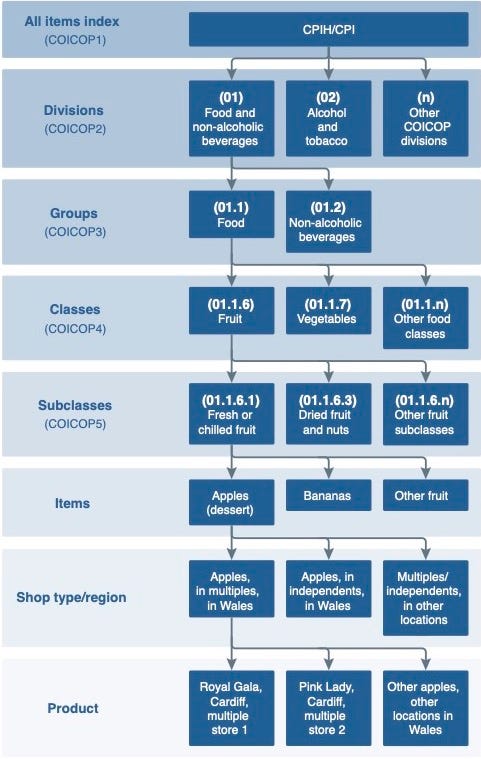

CPI covers about 700 individual products which are then sorted into ever more expansive indices:

At each level, each sub-category (e.g. ‘Fresh or chilled fruit’) has a weighting. The total weighting adds up to a 1000. So the weightings of all the subclasses added up = 1000. The weightings of all the groups = 1000 and so on.

This is the current breakdown of weightings for the 12 divisions - the level just below the overall CPI index:

These weightings change over time as spending habits and tastes change. In the UK this is done twice a year. First in January when adjustments are made for changes in expenditure (e.g. if rent becomes a much bigger part of total expenditure over time then it should impact the CPI more and more). And then again in February when the weightings change to take account of changing consumer habits.

When calculating the Index these changes in weights must be taken account of. This is done by ‘chain-linking’ in January and then again in February.

Obviously it would be impossible to include every single product or item so my model includes all divisions, sub-groups and the most relevant classes (such as electricity and gas).

In all cases from classes upwards, the correct double chain-linking is applied taking account of the changes to weights over time.

Limitations

For the moment we do not have the new weights for 2023 which may impact these forecasts. When the new weights are released in February I will update these predictions. The most important thing to watch out for is how the new weights impact the contribution from energy prices to inflation.

Because I’m not working up from the product or item level, there will be some gap between the assumptions I’ve plugged in and how they will really appear. There is no way round this but I think that these errors should be minimal looking at how changes to particular items in previous years impacted higher level indices.