UK: An inflation outlier?

Inflation has remained higher in the UK than in any other major economy:

Markets are coalescing behind the view that this isn’t just a blip but a structural break that is going to take several years (and much tighter monetary conditions) to unwind:

The strength of this demarcation has surprised me but so have the recent disappointing inflation prints. I’m feeling increasingly lonely in the ‘transitory for longer’ camp.

Here I try and break down the inflation picture in the UK to assess whether the UK is really different, or merely lagging behind the mild disinflation1 that most other parts of Europe are starting to see.

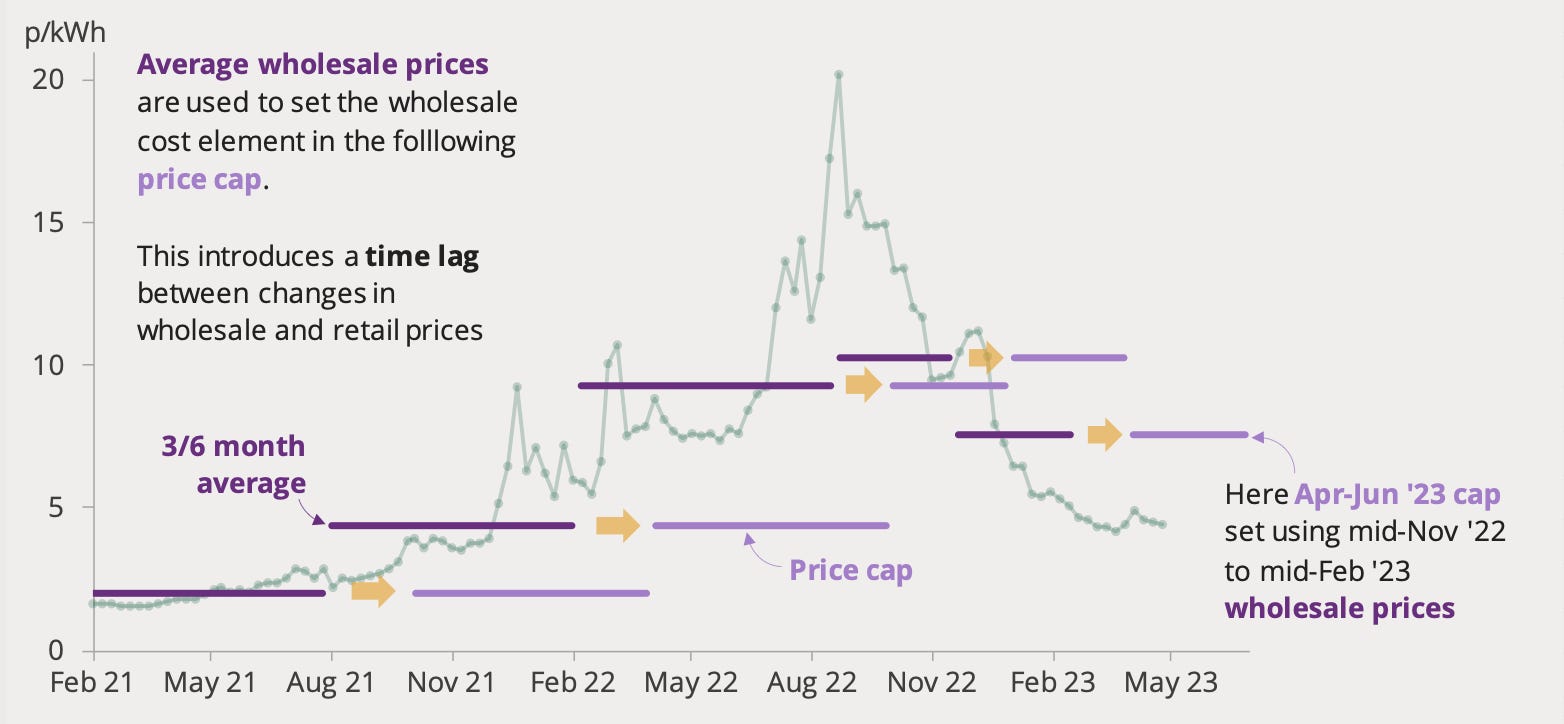

The most important place to start is the huge energy shock that the UK has experienced. Because of the UK’s very large reliance on natural gas, and because of the 3 month tariff structure that businesses and households face, the UK has had a larger and more prolonged shock than other European countries:

In a New-Keynsian model with real rigidities in the labour market, this larger and more prolonged shock is important beyond just the direct contribution to inflation. The greater and the more prolonged the shock, the greater the wage demands of workers who are trying to maintain their prior real income levels. This then feeds into higher prices and then higher wages and prices and so on. The supply shock creates inflationary momentum beyond the initial rise in prices.

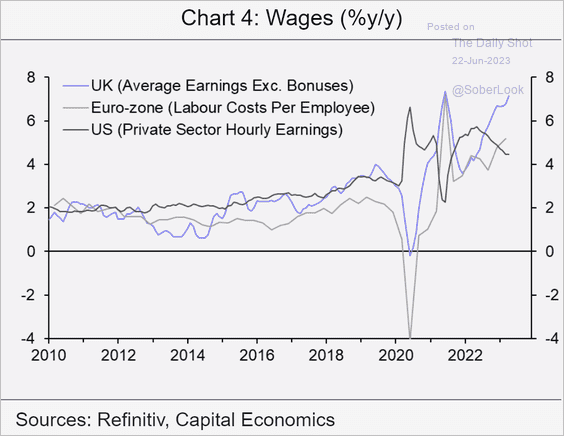

We have probably seen this play out in the UK where wage growth has been higher2 than in Eurozone countries that experienced smaller and shorter energy shocks:

These inflationary wage dynamics have been accentuated by the tightness of the UK labour market which has given workers more power to demand these wage increases. The UK labour market was always tighter than in most of Europe3 pre-COVID but has become more so after the end of freedom of movement4 and because of major problems in the healthcare system:

Together this has reduced the participation rate and massively increased vacancies:

Without access to an expensive data platform I can’t do a good graphical comparison with other European countries, but the UK is definitely unique in having a combination of all of

a) a lower participation rate than before COVID (although now quickly recovering)

b) Vacancies significantly above pre-COVID levels

c) An unemployment rate at, or below 4%. By comparison, in France it’s 7.1%. In Germany it’s 5.7%. In Italy it’s 7.8%. In Spain it’s 13.3%

In sum, the energy shock has been bigger and longer and its translation into further inflationary momentum has probably been aided by a tighter labour market than in comparable European countries. But how much of this represents a permanent structural break between the UK and the Eurozone, and how much of it will just unwind on its own?

The first thing to look out for is energy and food dropping out of the inflation numbers and actually providing some deflationary drag. We should expect this to happen over the next 6-12 months:

Beyond the direct effect, these falls should help drag down expectations among workers and price setters. These are the prices that people really notice. In theory, workers should then dampen future wage demands helping to reverse a decent chunk of the initial inflationary momentum that was created. To the extent that this happens, the UK is just a laggard and not experiencing anything more dangerous than other European countries.

But there are definitely reasons to worry that things won’t be that simple.

One worry is that Central Bank credibility has taken a bigger hit in the UK because of the length of the shock, overly dovish communications from the Bank, and a large degree of political turmoil in recent years (Brexit, Truss Mini Budget). The danger is that inflation expectations are becoming de-anchored in a way that they aren’t in the Euro Area, making it more difficult to bring inflation back to target. Personally I’m not overly worried by this channel. I think the end of inflation in food and energy will matter much more to actual wage and price setting than investor worries about Central Bank credibility, but it’s definitely an open question.

A bigger risk in my view is continued structural tightness in the labour market. In an interesting paper, Bernanke and Blanchard argue that the inflation generated by labour market tightness can be more dangerous than the inflation originating from a price shock, as it can build over time. This is made much more dangerous if expectations really have de-anchored (in red)5:

Being optimistic, the labour market seems to be showing some very early signs of weakness but its taking longer than many expected:

It’s also hard to know how much of this weakening is due to tighter monetary policy and how much can be attributed to structural loosening as the economy gets used to the new post-Brexit migration system.

In conclusion, I think the falls in energy and food inflation will do a lot of the work in bringing inflation down from its highs. In that regard the UK is just lagging behind other economies. The structure of the labour market is the big differentiator. The extent to which the labour market does, or does not adjust, could play a significant role in the pace of disinflation as well as how the UK fares in the face of any subsequent supply shocks.

Some countries like Spain have seen a rapid fall in headline inflation but core inflation rates are still above target and falling less quickly.

And we have seen severe strike activity which suggests this real wage rigidity is playing an important role. Especially after stagnant wage growth since 2008, workers and unions are very determined not to be the losers from the price shock.

In terms of unemployment.

While net migration is up quite a lot, the type of migration has changed. Flexible ‘un-skilled’ labour is much harder to come by as the new visa system doesn’t allow for people to come to the UK for these jobs by default. This has probably created expensive wage adjustments in particular sectors.

Obviously I don’t want to over claim here. The shape and position of the Philips curve, as well as whether or not it is in some way state-dependent is highly contested. That said, I think it’s reasonable to assume that when the labour market is very tight on multiple measures (unemployment, wage growth, beverage curve), the risks of inflation generated by a tight labour market need to be taken seriously.